واحد تجاری ساختاریافته: یک واحد تجاری است که بهگونهای سازماندهی شده است که حق رأی یا سایر حقوق مشابه، عامل اصلی در تعیین کنترلکننده واحد تجاری نیست، مانند زمانی که حق رأی تنها در ارتباط با وظایف اداری است و فعالیتهای مربوط از طریق قرارداد هدایت میشود. در بندهای ب22 تا ب24 (به شرح زیر) اطلاعات بیشتری درباره واحدهای تجاری ساختاریافته ارائه شده است. (استاندارد حسابداری 41 افشای منافع در واحدهای تجاری دیگر (مصوب 1398))

ب22. یک واحد تجاری ساختاریافته، اغلب از برخی یا تمام ویژگیها و خصوصیات زیر برخوردار است:

- الف. فعالیتهای محدود.

- ب. هدف محدود که به خوبی تعریف شده است، مانند انعقاد قرارداد اجاره دارای صرفه مالیاتی، انجام فعالیتهای تحقیق و توسعه، فراهم کردن منبع سرمایه یا تأمین مالی برای واحد تجاری یا فراهم کردن فرصتهای سرمایهگذاری برای سرمایهگذاران از طریق انتقال ریسکها و مزایای مرتبط با داراییهای واحد تجاری ساختاریافته به سرمایهگذاران.

- پ. حقوق مالکانه ناکافی که به واحد تجاری ساختاریافته اجازه تأمین مالی فعالیتها بدون حمایت مالی تبعی را نمیدهد.

- ت. تأمین مالی برای سرمایهگذاران به شکل ابزارهای متصلشده به یکدیگر از طریق قراردادهای چندجانبهای که تمرکز ریسک اعتباری یا سایر ریسکها را ایجاد میکنند.

ب23. نمونههایی از واحدهای تجاری ساختاریافته به شرح زیر است، اما محدود به این موارد نیست:

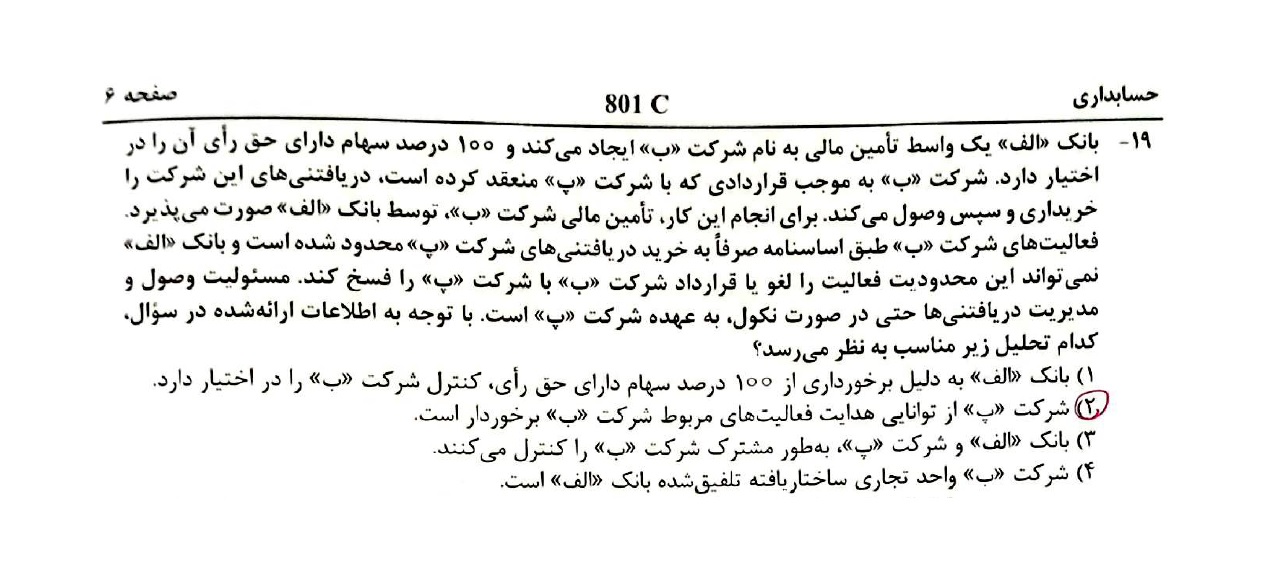

- الف. واسطههای تأمین مالی. (مشابه سوال 19 حسابداری در آزمون انتخاب حسابدار رسمی سال 1404 (به شرح زیر))

- ب. تأمین مالی به پشتوانه دارایی.

- پ. برخی صندوقهای سرمایهگذاری.

ب24. یک واحد تجاریکه از طریق حق رأی کنترل میشود، واحد تجاری ساختاریافته محسوب نمیشود، زیرا برای مثال، تجدید ساختار این واحدها به سهولت توسط اشخاص ثالث تأمین مالی میشود. (استاندارد حسابداری 41 افشای منافع در واحدهای تجاری دیگر (مصوب 1398) - پیوست ب: رهنمود بکارگیری)

|

structured entity: An entity that has been designed so that voting or similar rights are not the dominant factor in deciding who controls the entity, such as when any voting rights relate to administrative tasks only and the relevant activities are directed by means of contractual arrangements. - IFRS 12 Disclosure of Interests in Other Entities

Paragraphs B22–B24 provide further information about structured entities.

B22. A structured entity often has some or all of the following features or attributes

|

B23. Examples of entities that are regarded as structured entities include, but are not limited to

|

B24. An entity that is controlled by voting rights is not a structured entity simply because, for example, it receives funding from third parties following a restructuring. |

دیدگاه خود را بنویسید